A new generation of high-quality office buildings is appearing, reflecting a growing focus of demand for space that goes the extra mile. And, despite the challenging economic conditions, occupiers are willing to pay the premium.

Download the Regional Office Market Report in full 2023 here →

The events of recent years have driven increased demand towards very high-quality office space. While this trend was arguably already in train, it has been accelerated by the experience of the pandemic. Increased hybrid working is prompting a growing number of occupiers to exchange quantity for quality, while premium workspace is playing a key role in attracting staff into the office.

The arrival of so-called prime office buildings into the regional markets has driven rents onto benchmarks that until recently were considered unthinkable. Typically, the prevailing economic environment is a key influence on rental growth, but recent trends reveal a clear disconnect. Reflecting this structural evolution in demand, strong prime rental growth is now taking place despite challenging conditions in the economy.

Across all 20 regional markets, prime headline rents are set to rise by an average of 5.5% during 2023 (including the forecast for Q4), the strongest annual growth in 16 years. Notably, this increases to an average of 7.1% across the Big Six, reflecting the focus of prime supply in these markets.

In contrast, reflecting growing polarisation of the demand between the best and the rest, growth in the wider office market is sluggish by comparison - average rental growth on MSCI’s regional offices segment is on course to hit a modest 1.3% in 2023.

PRIME DEFINED

So, what does a prime office building look like? While no two buildings are the same, prime offices need to embody several certain attributes which set them apart from more conventionally defined grade A specified buildings.

First, prime buildings must boast strong ESG credentials. Low operational carbon impact in the form of A or B-rated EPC certification is a given, with more environmentally encompassing accreditations such as BREEAM and NABERS ratings now typical. Additionally, accreditations more closely associated with the physical quality of the workspace and staff wellbeing are becoming commonplace, notable examples including WELL and FITWEL.

However, to really qualify as prime, an office also needs to offer a mix of high-quality amenities. There is no standard approach to amenity provision, and one prime building may offer a different scope of amenity to another to help differentiate the product to the market.

Generally, outside space is now highly sought after, in particular roof terraces with associated hospitality / café facilities, while ‘spa-quality’ changing facilities and gyms often feature at basement level. A proportion of many prime buildings may also be allocated for shared workspace, allowing occupiers a greater degree of flexibility.

Provided it has the necessary attributes, a prime office can be either new build or refurbished. This is evidenced by the fact some back to frame refurbishments have proven capable of driving prime headline rental growth in the markets into which they have been delivered. Indeed, given the lower embodied carbon associated with refurbishments, such schemes offer an added benefit to occupiers looking to demonstrate a strong commitment to environmental sustainability.

PRIME SUPPLY IS LIMITED

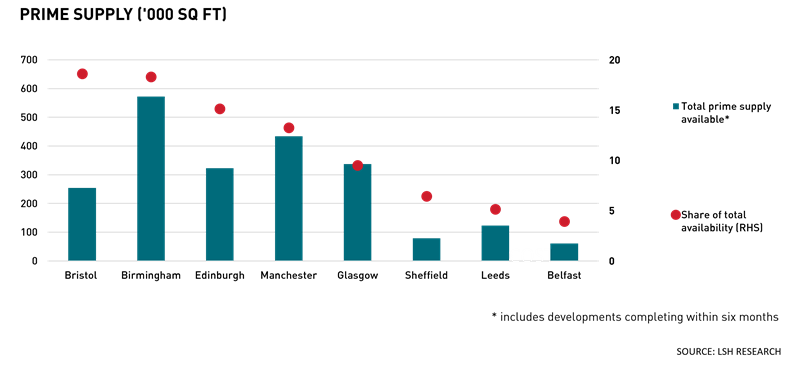

At this point in the evolution of the office market landscape, the strong rental growth exhibited by prime buildings partly reflects their scarcity. While total supply has increased across the regional markets, the amount that qualifies as prime, at 2.2m sq ft, accounts for only 26% of grade A supply and 9% of overall supply. Furthermore, 94% of prime supply is concentrated in the Big Six city centre office markets.

Birmingham is presently a key focus of prime supply, with availability of 572,000 sq ft making up 18% of the total. Proportionally, Bristol and Manchester city centre also offer a reasonable degree of choice, with prime supply making up 19% and 13% of total supply respectively. Leeds is the main outlier among the Big Six, with prime supply accounting for only 5% of the total and spread across four buildings.

While locations such as Cardiff, Newcastle and Nottingham are so far devoid of a prime scheme, some of the UK’s smaller regional markets have some degree of prime availability. For example, Sheffield (78,514 sq ft across two schemes) and Belfast (61,193 sq ft total across two schemes) do have a limited amount available, albeit accounting for a relatively minimal 6% and 4% of total supply respectively.

THE RACE FOR SPACE

While the delivery of prime buildings is a relatively recent phenomenon, part of the reason for the current scarcity is the sheer weight of seen appetite for them. Many schemes that have been delivered over the past two years have been taken-up aggressively, and often attract occupiers to sign up prior to their completion.

Perhaps the best example is MEPC’s 11/12 Wellington Place in Leeds city centre, where all 200,000 sq ft has already been let prior to its scheduled completion in Q1 2024. This scheme was home to the largest regional deal of the year, with Lloyds Banking Group pre-letting 124,400 sq ft shortly after construction commenced.

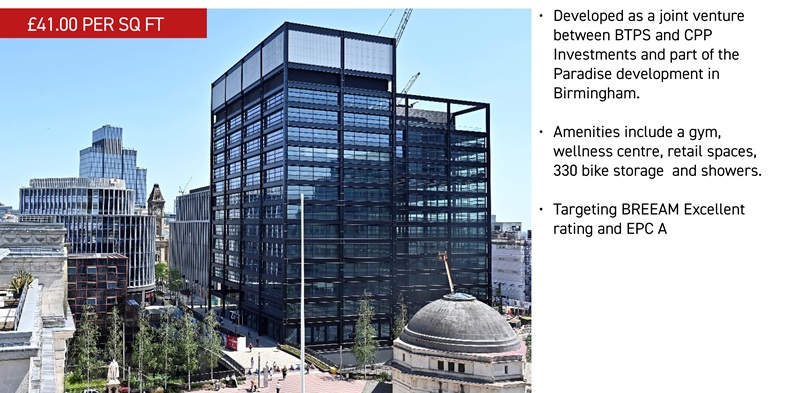

Similarly, MEPC and Federated Hermes’ One Centenary Way, Paradise, Birmingham has already seen a number of high profile lettings. The 286,000 sq ft scheme completed in Q1 2023 and is already 70% leased. Again, this featured one of largest regional office deals in recent years, namely Goldman Sachs’ 100,000 sq ft pre let deal in Q3 2022.

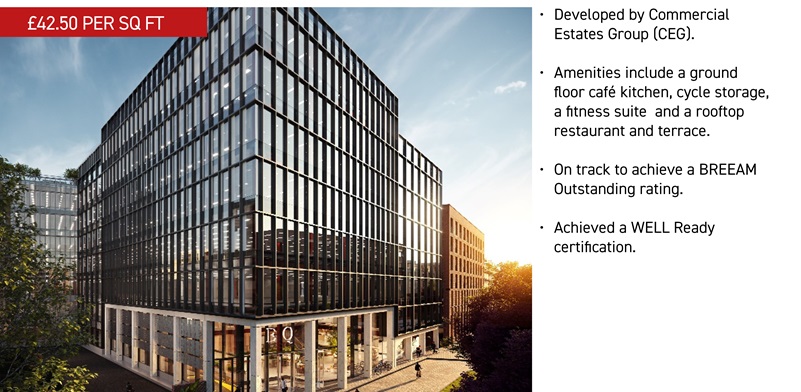

A more recent development is CEG’s EQ in Bristol, where the 205,000 sq ft scheme includes circa 20,000 sq ft of amenity-related space. Completing in Q4 2023, the scheme has already received strong demand, highlighted by Evelyn Partners’ 27,406 sq ft recent pre-let. Notably, EQ’s top floor is set to push Bristol’s prime headline rent up to £45.00 per sq ft.

WIDENING THE GAP BETWEEN BEST AND REST

Despite a likely continuation of sluggish economic conditions in 2024, focused demand on a limited supply of prime buildings is expected to drive continuing rental growth over the medium term. Regional prime headline rents are forecast to increase by a further 5.1% per annum to 2026, in comparison with only 1.3% per annum on MSCI’s equivalent average, further accelerating the polarisation between the best and the rest across the regional markets.

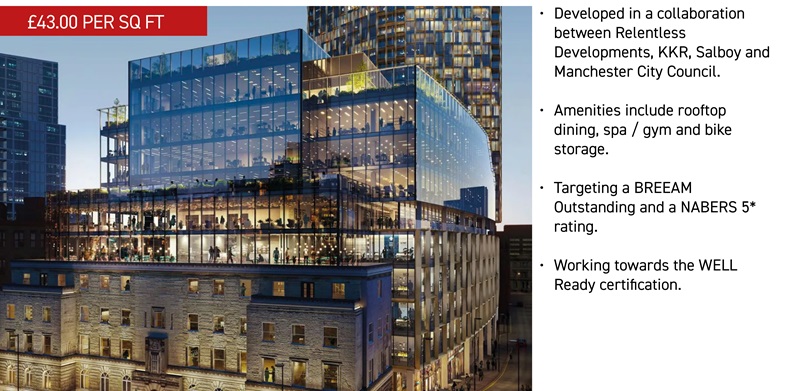

Expectations of continuing growth are largely driven by the prime schemes in the pipeline that are expected to complete in the next two years. Most notably, Manchester, Birmingham and Bristol all have prime space completing over the next two years. This includes No 1 St Micheal’s (186,000 sq ft) and The Alberton (220,000sq ft) in Manchester, The Drum (200,000 sq ft) in Birmingham and The Welcome Building (206,000 sq ft) in Bristol.

OPPORTUNITY KNOCKS

While the office sector has gone through a painful period of pricing adjustment, occupiers’ increased focus on quality in the wake of the pandemic is generating a wave of opportunity across the UK’s regional office markets.

Clear evidence that occupiers are willing to pay a premium to secure the very best space is crucial towards ensuring viability as the market moves into a new cycle. To date, the core regional cities have understandably blazed a trail, reflecting critical mass in those markets and investors’ perceptions of lower risk that comes with it. However, in time, the trend is sure to ripple out more substantively to other key regional markets, driving rents to a level that can enable a new tranche of development to come forward.

ONE CENTENARY WAY, PARADISE, BIRMINGHAM

NO 1 ST MICHAEL'S, MANCHESTER

EQ, BRISTOL

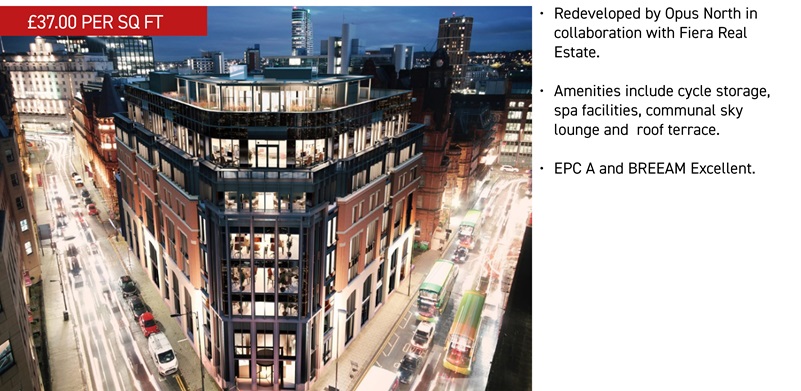

12 KING STREET, LEEDS

Download the Regional Office Market Report in full 2023 here →

Related Content

REGISTER FOR UPDATES

Get the latest insight, event invites and commercial properties by email