Underpinned by up to £16bn of public financial capacity, the Bank represents one of the most significant structural interventions in housing finance for a generation.

For LSH clients - including local authorities, developers, investors, and delivery partners - the announcement is more than a headline. It signals a fundamental shift in how we can bring forward together stalled sites, viability challenges, and infrastructure‑heavy regeneration schemes over the coming decade.

WHAT IS THE NATIONAL HOUSING BANK?

The National Housing Bank opened for business on 1 April 2026, operating as a subsidiary of Homes England and headquartered in Leeds. It has been established as a permanently capitalised public finance institution, enabling it to take longer‑term, more commercial views on risk than previous government funding programmes.

The Bank has the ability to deploy up to £16bn through a mix of:

- Debt

- Equity

- Guarantees

Its stated ambition is to:

Crucially, the NHB has been designed to crowd‑in private investment, rather than replace it. Its role is to “make the unviable viable”, targeting those schemes that struggle to progress under current market conditions, rather than schemes that would proceed anyway.

WHAT TYPES OF CHALLENGES IS THE BANK AIMING TO SOLVE?

The National Housing Bank is explicitly targeted at well‑understood market failure points. These include:

- Stalled or marginal sites where abnormal costs undermine viability

- Upfront infrastructure requirements that delay development

- SME housebuilder finance constraints

- Brownfield and urban regeneration schemes

- Places that have historically struggled to attract institutional capital

In practice, this means schemes that combine housing delivery with wider regeneration, including town centre renewal, remediation, transport, or utilities investment, are likely to be central to the Bank’s activity.

The NHB will also work through Homes England’s regional and mayoral engagement model, strengthening the role of place‑based partnerships and locally led pipelines.

The key question now is not what the National Housing Bank is, but what difference it will make to real projects on the ground.

EARLY SIGNALS: FROM POLICY TO DELIVERY

The launch was accompanied by immediate evidence that the Bank is operational, not theoretical. Since opening for business, the NHB has announced two early commitments:

- a £100m institutional investment partnership with Aviva, and

- a multi‑million‑pound debt facility with land promoter Richborough.

Together, these illustrate the Bank’s ability to intervene across different stages of the housing delivery pipeline.

Institutional investment: Aviva (announced 31 March 2026)

Type: Institutional investment platform

NHB role: Capital deployed through the NHB as part of its launch

Details: £100m initial commitment; up to 3,300 build‑to‑rent homes starting in Liverpool and Manchester

Status: First announced NHB partnership at launch

Early‑stage pipeline acceleration: Richborough (announced 8 April 2026)

Type: Multi‑million‑pound debt facility for land promotion and planning

NHB role: Explicitly confirmed as “one of the first commitments made through Homes England’s newly established National Housing Bank”

Details: Supports early investment in land and planning applications; accelerates supply of consented sites for SMEs, RPs, and major housebuilders

Status: First clearly announced early‑stage / pipeline NHB intervention

What these early deals tell us

Taken together, the Aviva and Richborough partnerships send a clear message to the market:

- The National Housing Bank is open for business

- It is prepared to support different partners, products, and stages of delivery

- It is focused on systemic impact, not one‑off, ad‑hoc interventions

- Housing delivery and regeneration are being approached as a whole pipeline challenge, from land and planning through to long‑term investment and delivery

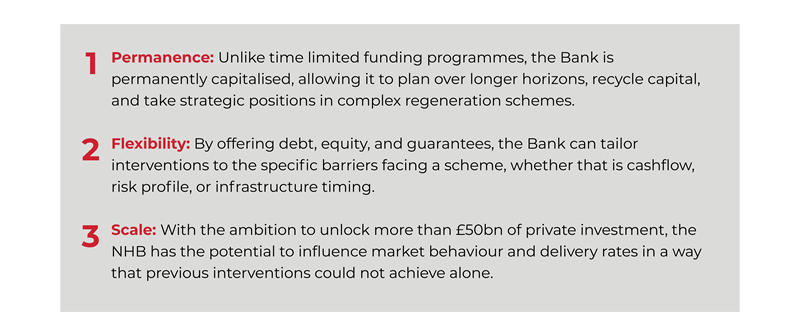

WHY THIS REPRESENTS A STEP CHANGE

While Homes England has long played a critical role in housing delivery, the National Housing Bank introduces three material differences.

LSH INSIGHT: WHAT THIS MEANS FOR CLIENTS

With 1.3m people trapped on social housing waiting lists it is essential that this new initiative is supported to achieve its aim of addressing the lack of quality and affordability within the national housing market. In doing so it is envisioned that there will be a positive impact on economic growth and it should help deliver 176,000 children out of temporary accommodation.

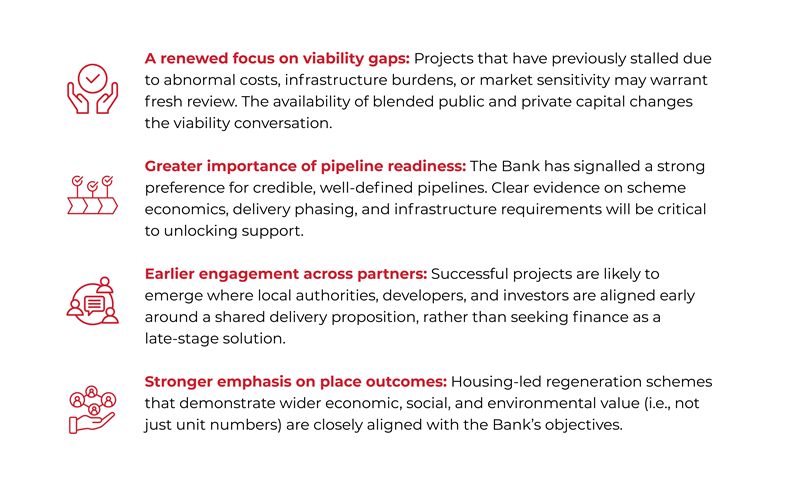

The National Housing Bank creates a new set of opportunities, and expectations, for places and delivery partners.

For LSH clients, the practical implications are likely to include:

At LSH, we are supporting clients across the public and private sectors to translate the National Housing Bank’s ambitions into delivery‑ready propositions, from reviewing stalled or marginal schemes, to strengthening viability evidence, shaping place‑based regeneration narratives and positioning pipelines for early engagement with Homes England and the National Housing Bank.

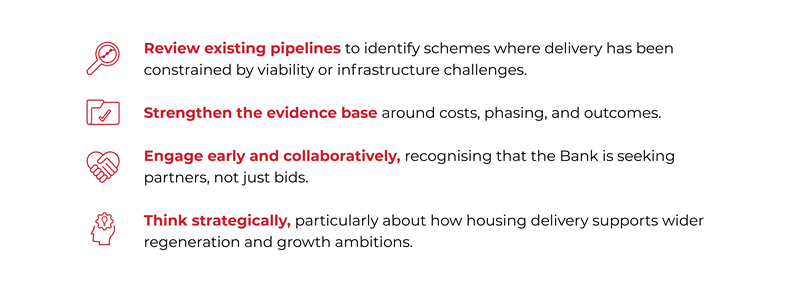

WHAT SHOULD PLACES AND PARTNERS BE DOING NOW?

As the National Housing Bank moves from launch into early delivery, there are some immediate actions for places to consider.

A NEW OPPORTUNITY FOR HOUSING‑LED REGENERATION

The creation of the National Housing Bank marks a significant shift in the government’s approach to housing and regeneration finance. It reflects a recognition that accelerating delivery at scale requires new tools, longer‑term thinking, and stronger partnerships between the public and private sectors.

For places grappling with viability challenges, infrastructure constraints or stalled regeneration sites, the NHB offers a potentially transformative opportunity - provided projects are well‑positioned, evidence‑led, and ready to engage.

As the Bank builds momentum, converting a national announcement into local impact will depend on the quality of pipelines, partnerships, and propositions brought forward; an area where early strategic advice and evidence‑led positioning will be critical.Related Content

REGISTER FOR UPDATES

Get the latest insight, event invites and commercial properties by email