The valuation industry has responded well to the extraordinary challenges posed by the COVID-19 pandemic, and lessons learned from lockdown are aiding the evolution of an increasingly collaborative and flexible profession.

The COVID-19 crisis has presented the UK’s valuations profession with unprecedented challenges. Valuers have been well-supported by RICS, which has issued regularly-updated guidance that has assisted the continued delivery of Red Book standard valuations, even at the height of the lockdown. However, valuers have needed to be agile in order to provide reports in spite of unique practical and methodological difficulties.

Valuing in lockdown

Lockdown brought immediate practical challenges, most obviously by making site visits impossible in many cases. Operating under government guidelines, LSH’s Valuations team never completely stopped making inspections during lockdown; for example, it remained possible for locally-based valuers to inspect some properties that had been vacant for more than 72 hours. However, an inevitable consequence of lockdown was an increased reliance on desktop valuations, drive-by inspections and information gathered from historical valuation reports.

Throughout recent months, the onus has been on valuers to take a collaborative approach and work closely with clients to find solutions that address the constraints on inspections and valuations. The end product – the valuation report – has remained fundamentally unaltered, but flexibility has been needed in the methods used to create reports.

Although lockdown restrictions have now eased, collaboration with clients and flexibility over report methodologies remain essential to the valuations process, with inspections continuing to be affected by the need to operate safely within the government’s workplace guidelines.

Material uncertainty

A key part of RICS’ response to COVID-19 has been its guidance on material uncertainty. In March, it advised that it may be warranted to include material valuation uncertainty declarations in members’ reporting and advice. This was to provide clients with transparency of the fact that, due to the extraordinary circumstances, less certainty could be attached to valuations than would normally be the case.

The need for material uncertainty declarations stemmed from both the constraints on valuers’ abilities to conduct their work and the lack of market evidence since COVID-19 began to have its impact. With the UK investment volume dropping to a record low in Q2, there is almost a complete absence of recent comparable evidence in some parts of the market.

The RICS Material Valuation Uncertainty Leaders Forum has gradually adjusted the initial advice, by recommending that material uncertainty is no longer appropriate for a number of asset types. These initially included standalone food stores; industrial and logistics properties; institutional grade built-to-rent residential properties; and some assets with long dated annuity income. Most recently, in July, Central London offices and institutional grade student housing were added to this list.

However, the decision on whether or not to include a declaration of material uncertainty ultimately rests with the individual valuer, and should be judged on a case-by-case basis. Material uncertainty clauses are likely to remain in widespread use across many property types for some time and it is appropriate that a cautious and phased approach is taken to the easing of their use, given the widely varying levels of uncertainty in different property sectors.

Declining but divergent values

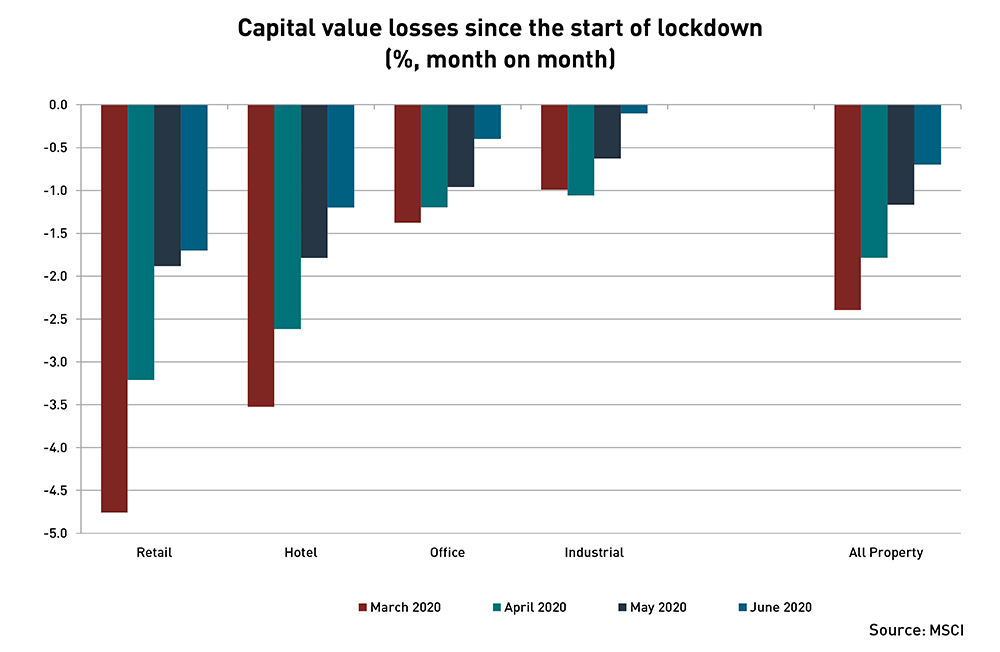

The differing impact of COVID-19 across the sectors is evident in MSCI data showing capital value movements since the start of lockdown. In the four months from March to June, all-property capital values fell by 5.9%, but there was a wide divergence between the sectors where businesses were hardest hit by lockdown restrictions such as retail (-11.1%) and hotels (-8.8%) and the more moderately impacted office (-3.9%) and industrial (-2.7%) sectors.

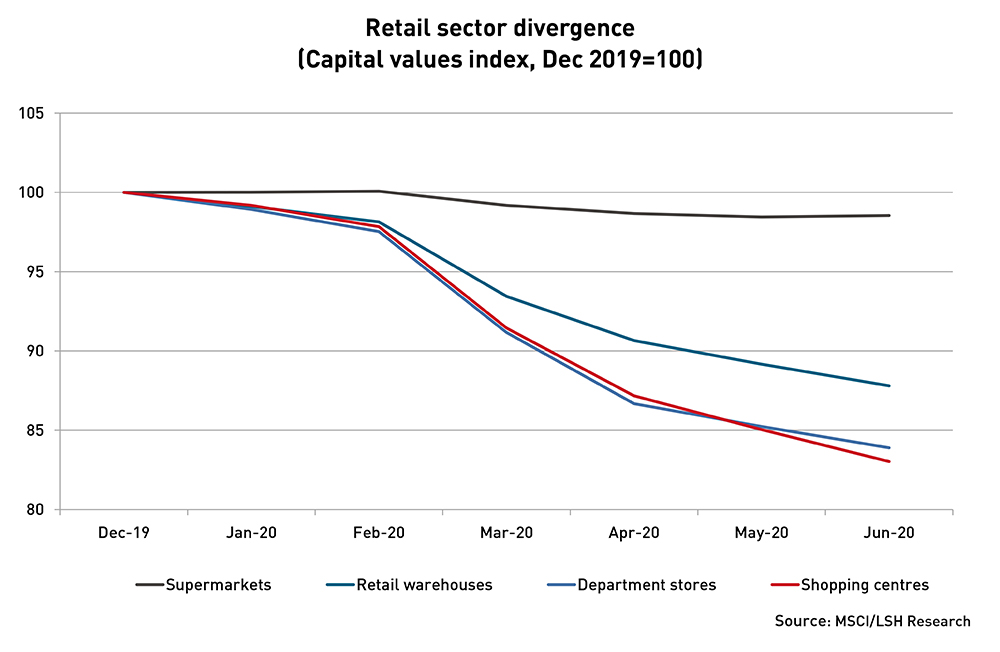

Even within the retail sector, the impact on capital values has varied greatly. Shopping centres, which were already the worst performing part of the commercial property market pre-lockdown, saw capital values fall by 15.1% in the four months to June, bringing the decline over the last 12 months to 25.5%. In contrast, supermarkets, which were able to remain open during lockdown, saw values drop by just 1.5% in four months.

Market evidence seen by LSH’s Valuations team has confirmed that falls in capital values have accelerated in the parts of the retail sector that were already struggling prior to lockdown. However, a much less consistent picture is visible in the office sector; some recent transactions have provided evidence of prices being chipped, while others have not.

The full impact of COVID-19 on office values may only become clear over the long term, as it will take time for occupiers to assess and adjust their office needs in response to increased home working. It is possible that a two-tier office market emerges, with values diverging between new grade A stock and older grade B properties.

Across all sectors, further downward adjustments to capital values are possible in the coming months as more evidence is gathered from transactions and quarterly rent collections. As a result, movements in property values may lag behind the wider economic recovery; while GDP growth has already begun to improve on a month-on-month basis after the very sharp shock of a 20.3% fall in April, it could be months before property values start to trend upwards.

The future of valuations

Regardless of its impact on property values, lessons will have been learnt by valuers from the lockdown period. Perhaps most importantly, the valuations profession has shown that it can function perfectly well without requiring staff to spend most of their time in a central office hub, and that there is a significant advantage in having a widely spread network of regionally-based valuers able to respond to client needs in different parts of the country.

Ultimately, COVID-19 may not result in wholesale change within the valuations industry, but it has already played a role in the evolution of an increasingly collaborative, nimble and flexible profession.

Related Content

REGISTER FOR UPDATES

Get the latest insight, event invites and commercial properties by email