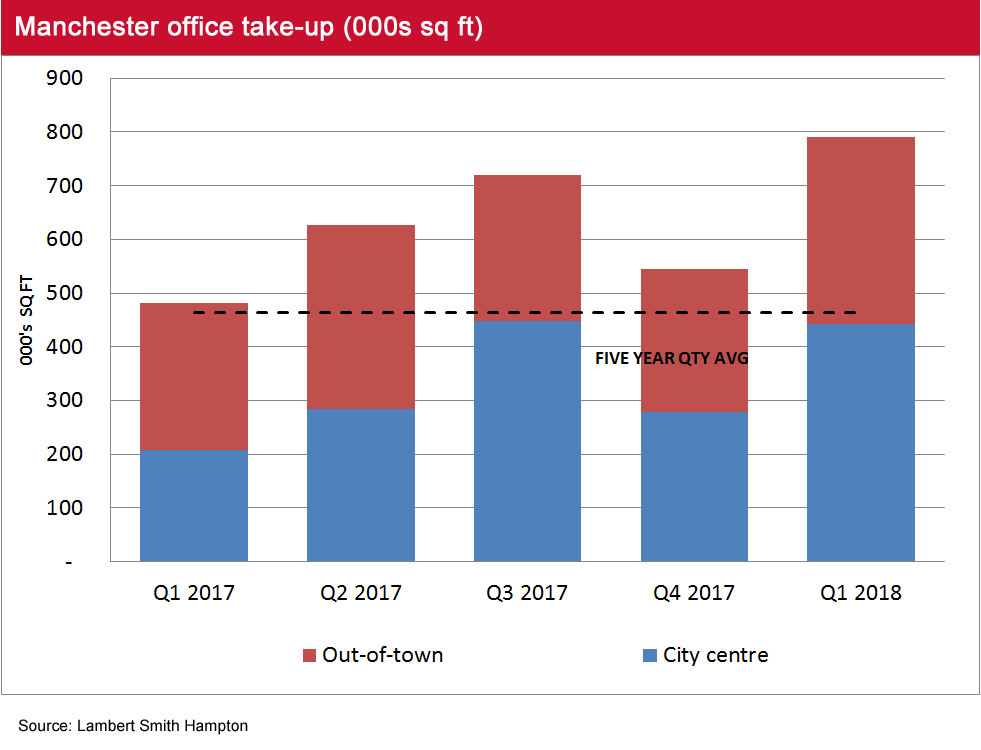

We saw an impressive start to the year. Manchester City Centre, South Manchester and the combined Salford Quays/Old Trafford markets have more than doubled their take-up figures when compared to the same quarter in 2017, providing a great foundation to build upon for the rest of the year.

An impressive start to the year

- City centre office take-up for Q1 2018 reached 435,590 sq ft across 81 transactions, which is more than double the figure achieved in the same quarter in 2017.

- Although more than a third of the total take-up (157,000 sq ft) related to one transaction, the GPU/HMRC committing a pre-let to Three New Bailey, the first quarter of 2018 is still very positive.

- Other notable transactions in Q1 included: 33,382 sq ft to Irwin Mitchell at One St Peter’s Square, 15,150 sq ft to Codethink Ltd at Helical’s newly refurbished 35 Dale Street and 12,540 sq ft to WorkLife at Core, Brown Street.

- In the out of town markets, take-up in South Manchester reached 169,170 sq ft in Q1, a 27% increase on Q1 2017. A big contribution came from The Hut Group which took a total of 40,283 at 4M at Manchester Airport.

- The combined Salford Quays and Old Trafford take-up figure equated to 81,747 sq ft, which is a 64% increase on Q1 2017.

- Although Warrington saw a 20% decrease on the previous year’s Q1 figure, with a total of 70,680 sq ft transacted, this is still seen as good quarter given the lack of delivery of new stock to the market.

Grade A appetite continues into 2018

- The occupier appetite for both grade A space – both new build and refurbished - has not slowed down with one 157,000 sq ft pre-let deal and 58,887 sq ft of grade A new build being taken up across four transactions.

- 55,410 sq ft of refurbished stock was also transacted across seven deals.

key occupational transactions

| Property | Size (sq ft) | Landlord(s)/vendor | Tenant |

| Three New Bailey | 157,000 | English Cities Fund | GPU/HMRC |

| 4M (Manchester Airport) | 40,283 | MAG | The Hut Group |

| One St Peter's Square | 33,382 | DEKA | Irwin Mitchell |

| 35 Dale Street | 15,150 | Helical | Codethink Ltd |

| Core, Brown Street | 12,540 | Boultbee Brooks | WorkLife |

| One St Peter's Square | 11,309 | DEKA | CBRE |

Source: Lambert Smith Hampton

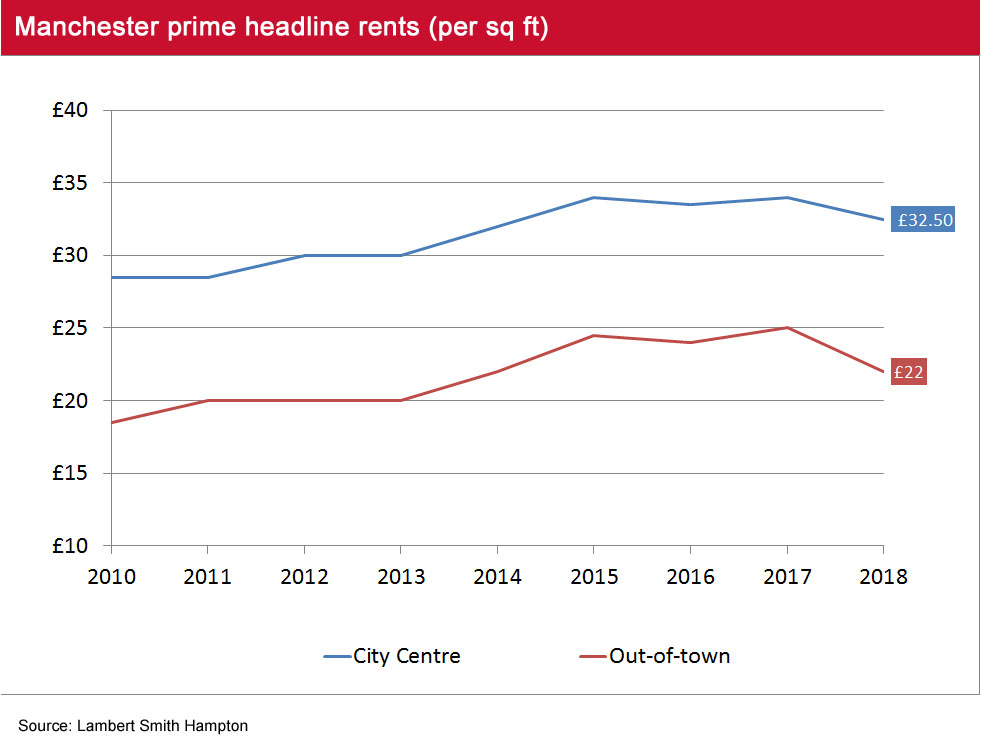

Prime rents remain stable

- The highest rent achieved within the city centre this quarter was at No.1 Spinningfields at £32.50 per sq ft closely followed by £31.50 per sq ft at One St Peters Square. We expect both headline rents and secondary refurbished rents to rise throughout the year with new build grade A supply continuing to diminish.

- Incentive packages remain low with on average a 9-12 month rent-free package being offered for a five-year term.

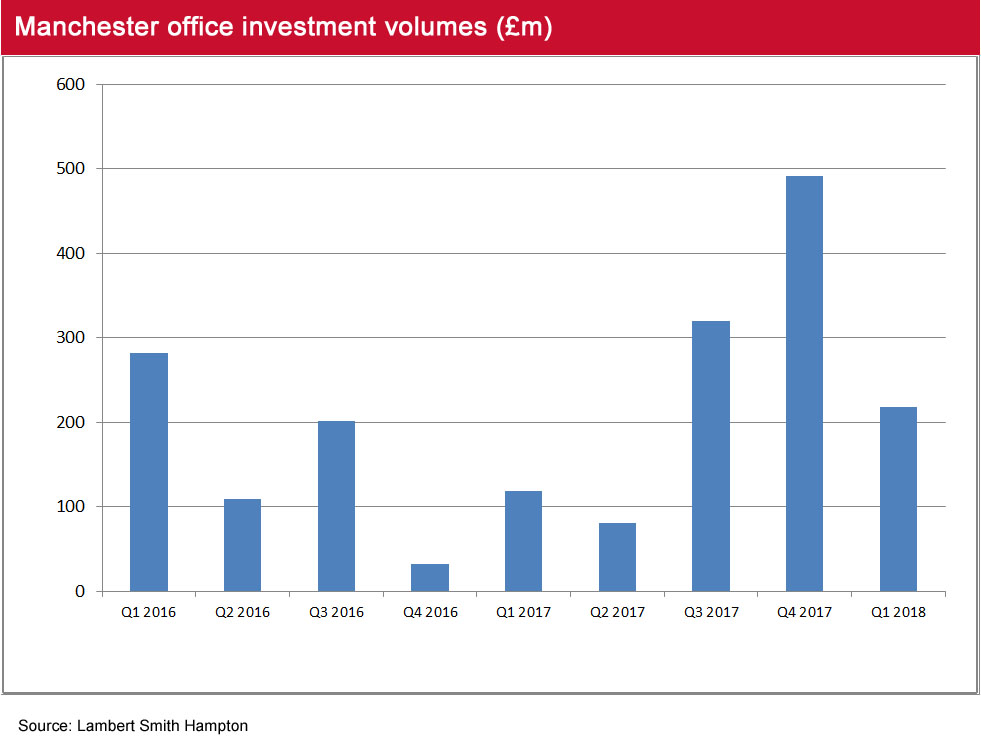

Investment activity

- Greater Manchester office investment activity totalled £218m in Q1 2018. This was an increase of £99m on the previous year but is down £273m on the final quarter of 2017.

- In Manchester city centre there were four key transactions which totalled £210m and accounted for 96% of the total volume.

- Aviva was the most active buyer, purchasing 2 New Bailey for £113m and 11 York Street for £50m.

- Other key deals included The Meridian, which was acquired by Fidelity UK Real Estate for £24.5m, and the £22.5m purchase of 81 Fountain Street by Blackrock.

- These figures demonstrate the continued investor demand for office assets in Greater Manchester where there is a strong occupier market.

key investment transactions

| Property | Value (£m) | Investor | Vendor |

| 2 New Bailey | 113 | Aviva | English Cities Fund |

| 11 York Street | 50 | Aviva | Kier |

| 81 Fountain Street | 22.5 | Blackrock | Aprirose |

Source: Lambert Smith Hampton

Related Content

REGISTER FOR UPDATES

Get the latest insight, event invites and commercial properties by email