Northern Powerhouse Office Report 2019

Read extracts from our report which explores the latest statistics, forecasts and dominant trends for the key city centre and out of town locations within the Northern Powerhouse office market.

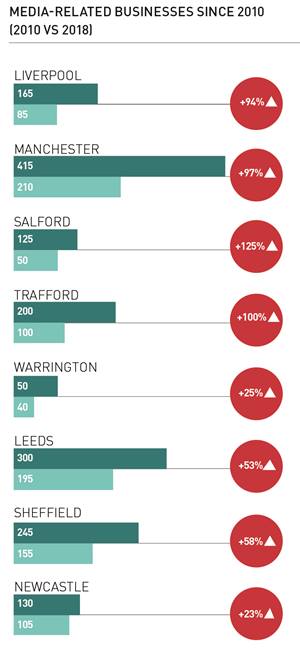

SECTOR FOCUS: MEDIA STORM

PROPERTY FOCUS: THE POWER OF KNOWLEDGE

PROPERTY FOCUS: SERVICED OFFICES

PROPERTY FOCUS: KEEP HS2 ON TRACK

OCCUPIER OVERVIEW: TMT ON THE CHARGE

INVESTMENT MARKET REVIEW: DEALING WITH INERTIA

SECTOR FOCUS: MEDIA STORM

The rapid growth of the media industry in the North is exciting and driving change across its key office markets. The proliferation of media businesses requires a different mindset from conventional development and investment approaches.

Channel 4’s decision to relocate its headquarters to Leeds has added to the growing perception that the UK media industry is moving northwards. However, the broadcast media has long had a presence in cities such as Manchester, Leeds and Liverpool.

What has changed is the proliferation of smaller media players in the region, with agile, talented staff capable of doing business for and with each other. In Manchester and Salford combined, the number of media businesses has risen by 128% since 2010, compared with 50% growth across the whole of the UK. The increasingly diverse nature of the North’s media industry is creating a range of new business opportunities throughout the region.

PRODUCTION HOTBEDS

Cities such as Manchester have a proud tradition of film and television production, with Granada TV and the BBC helping to make the city a hotbed of talent for over 50 years. The BBC’s decision to move large parts of its operations to MediaCityUK, Salford has acted as the catalyst for a new phase of growth in the Region. Now home to BBC and ITV operations, the Dock10 TV studios and over 250 smaller media and digital businesses, its growth has helped to solidify Greater Manchester’s status as the UK’s pre-eminent TV production hub outside London.

Channel 4’s move to Leeds will bring similar impetus to the city. Channel 4 has leased circa 26,000 sq ft at Rushbond’s Majestic scheme and will locate 250 jobs there by 2020. This is already helping to trigger further new developments with, for example, Leeds City Council backing plans for new film and TV studios at the former Polestar Petty printworks.

PROPERTY FOCUS: THE POWER OF KNOWLEDGE

Knowledge parks, or science and technology parks, have been growing across the UK over the last 30 years. These sites have spawned thousands of cutting-edge businesses over the years, while providing the educational support and contacts the next generation needs to keep innovating.

While knowledge parks have been around for some time, they have evolved over recent years. They have become far more specialised in terms of industry, in recognition that innovation relies on collaboration and clusters of expertise. Previously, an organisation loosely involved in any form of scientific or technological activity might choose to locate on one. Today, a park is likely to focus on one aspect, such as life sciences, food, health and wellbeing or cybersecurity. They are now catalysts for growth for niche industries.

The trick to developing a successful park, however, relies on the ability to see them through prospective tenants’ eyes.

THE GROWTH OF KNOWLEDGE PARKS

Almost all successful knowledge parks are established close to universities. These institutions provide the requisite talent, specialised expertise and the knowledge network. Indeed, many start-ups are founded by graduates who meet at university.

Universities themselves are keen to grow knowledge parks to communicate the success of their courses and students. In turn, the private sector is collaborating with universities and the public sector to establish and sponsor incubator spaces as a form of investment in future talent.

There are typically two types of knowledge parks across the UK: legacy builds and new builds. Most historic parks are legacy builds, where a large company created facilities then subsequently relocated, leaving a range of space and a cluster of highly-skilled staff which other organisations can utilise. There are fewer newly-built schemes, partly because the parks need critical mass to be successful as well as an anchor tenant or building to act as a catalyst to attract businesses and entrepreneurs. Creating a new cluster also requires a leap of faith as it’s highly unlikely that a start-up business/SME will allow sufficient time for a building to be built or will be attracted to the ‘traditional’ pre-let model.

Harwell Campus in Didcot is one of the UKs most successful legacy parks. Founded as an RAF facility, Harwell is steeped in world firsts: from the building of Europe’s first energy producing fission reactor to the launch of the transistorised computer.

Another successful park is Sci-Tech Daresbury in Warrington. The facility is internationally recognised in leading-edge research and development and is home to nearly 150 high-tech companies in areas such as advanced engineering, digital/ICT, biomedical and energy and environmental technologies.

Aerial photo of Harwell Campus, courtesy of Harwell Campus 2019

PROPERTY FOCUS: SERVICED OFFICES

The emphatic arrival of flex space operators in the North is no flash in the pan, and reflects the burgeoning growth in smaller businesses in recent years. As these operators lift the bar on quality, landlords of conventional space are increasingly adapting in order to compete.

MAKING WAVES

The region has seen a wave of flex space operators sweep in and take space over the past two years. If considered as a sector, serviced offices accounted for a substantial 10% of total take-up over the 12 months to Q3 2019, the third most active behind Technology, Media and Telecoms (TMT) and Finance, Insurance and Banking.

Manchester city centre has been the major focus of activity. Since the start of 2017, it has accounted for 64% of all flex space take-up across the eight key markets, its dominance boosted in 2019 with major deals including Spaces at 125 Deansgate (115,000 sq ft) and WeWork at Hyphen (51,000 sq ft).

However, demand is rippling out across the region’s other centres. Flex space operators have been a key driver of demand in Sheffield city centre in 2019, expected to account for around 15% of take-up for the year, while operators have also been active in Leeds during the year.

WHY NOW?

The structural change in office demand towards more flexible options is essentially driven by the internet revolution. The internet has eroded the traditional business benefits of scale, which in turn has fostered spectacular growth of small service sector businesses over the past decade. All this is highly conducive to demand for more flexible terms and collaborative working environments.

However, the recent spike of flex space take-up better reflects something of a race among operators and their respective investors to grab market share. Indeed, negative publicity around WeWork better reflects concerns over the sustainability of its business model, rather than the underlying occupier demand for flexible space per se.

Key Contact

PROPERTY FOCUS: KEEP HS2 ON TRACK

Cancelling HS2 will cost the North for years to come.

Amidst the headlines focusing on the General Election and Brexit, a root and branch review into the HS2 project is being carried out. As costs for the project have escalated wildly beyond the original £56bn budget and significant delays are expected, the appraisal is perhaps necessary; it will be the UK’s biggest rail infrastructure project for generations.

However, should HS2 be lost, northern regions will foot the bill for years to come Much of the northern rail network is built on Victorian infrastructure which is already either overloaded or close to being so. Throw regular delays and cancellations into the mix and rail travel down the spine of the country quickly becomes a misery of standing for hours or abandoning critical meetings on the way. As a colleague noted, a rebrand from HS2 to ‘Extra Capacity 2’ may be a better fit. in the currency of lost opportunity. The Northern Powerhouse Independent Review (NPIR), established to pre-empt the Government’s review of the project, has called for control of HS2 to be devolved to the North and Midlands and warned that its cancellation would remove all possibilities they have in transforming their economies. Pleasingly, in November 2019, a draft copy of the Government’s review determined that HS2 should be built, despite costs that it estimates could reach £88bn. But the project remains far from certain. The review’s deputy chair, Lord Berkeley, does not support it, saying the cost has not been properly scrutinised. If recent events have taught us anything, it is that nothing is off the table under the new political regime. To ensure the project stays on track, we must collectively make our voices heard. THE CASE FOR CAPACITY One of the principal criticisms of HS2 is its ‘all roads lead to London’ approach; that simply connecting major regional cities to the capital acts as a further drain on regional talent. This is most relevant to the Phase One line, which improves capacity on an already fairly rapid service from Birmingham. However, regardless of high speed, boosting capacity is becoming essential for the North.

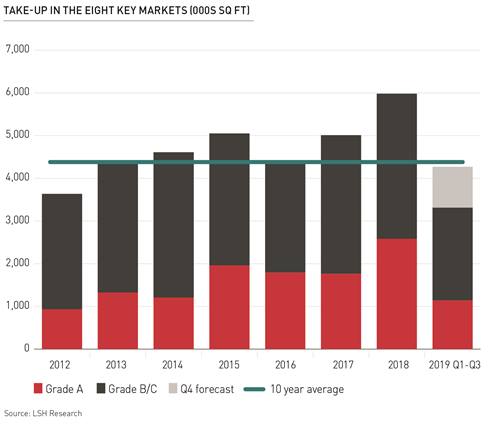

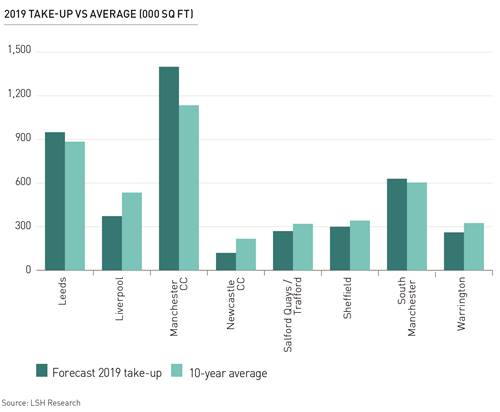

OCCUPIER OVERVIEW: TMT ON THE CHARGE

Against a backdrop of political uncertainty, Manchester and Leeds have boasted another strong year of activity in 2019. Supply has played a key role in driving activity, with limited choice of quality options in the region’s other key markets weighing on take-up.

Following record annual take-up in 2018, collectively, the eight key occupier markets of the Northern Powerhouse have experienced a solid if unspectacular year over 2019 to date. Over the first three quarters of 2019, total take-up of 3.3m sq ft is down 23% on the equivalent period last year but is marginally ahead of the average for the period.

The markets have arguably performed well in the face of two distinct challenges. Brexit has been an influence, with two, ultimately unsuccessful, attempts to depart the EU during the year interfering with occupiers’ location strategies. The other, arguably more crucial, factor is supply, with the majority of locations struggling to provide sufficient quantum and quality to drive take-up.

Key Contact

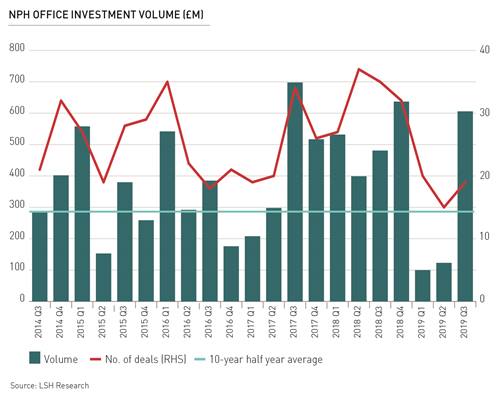

INVESTMENT MARKET REVIEW: DEALING WITH INERTIA

Despite impressive volume in Q3, the office investment market across Northern Powerhouse Cities has been characterised by inertia and indecision throughout 2019. However, the underlying fundamentals of the region’s occupier markets remain attractive, offering opportunities to create value when certainty returns.

A TALE OF TWO DEALS

After what can only be described as a poor first half of the year, office volume in the third quarter rebounded to such an extent that it realigned with the strong levels seen throughout 2017 and 2018 - at £637m, volume in Q3 was nearly four times that witnessed in H1. While welcome, this volume spike belies activity on the ground, with the number of transactions down by circa 50% compared with the same period in 2018.

Q3 volume was dominated by two substantial long-income deals in Leeds, both involving the same institutional buyer. In August, Legal & General purchased the Government Property Unit (GPU) hub 7&8 Wellington Place for £211m (NIY 4.3%) from Hermes REIM. L&G then acquired Quarry Hill House for £243m (NIY 3.15%) in September from RO Limited; another long-let product, this time to the NHS. With a combined value of £454m, the two deals accounted for more than half of the region’s entire office volume in 2019 to date.

7&8 Wellington Place, Leeds

Key Contact

Market insight

Download full report

Get detailed insight on demand, supply, rents and investment volumes on the region's the eight key office markets.

Download PDF

Market insight

Request a 1-2-1

Secure your bespoke presentation and discussion with one of our experts

Request 1-2-1

Offices to let across the Northern Powerhouse

Market insight

Get in touch

Email me direct

To: