Enquiries remain consistent

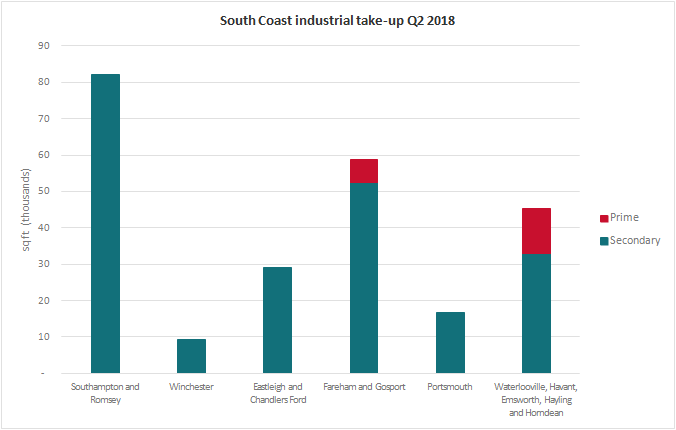

Q2 has witnessed a decline in take up

Take up in Q2 has witnessed a decline however, this can largely be attributed to a high number of large transactions that are currently under offer (totalling approximately 550,000 sq ft). We anticipate a significant number completing in the coming quarters, readdressing the drop in figures in Q2. Again take up this quarter has primarily been for secondary stock as occupiers take refurbished space and remain cost conscious, in addition to satisfying contract led, tight timescales, for occupation.

The vital statistics have been summarised below:

| Q2 2018 (sq ft) | Q1 2018 (sq ft) | % change | % change Year on Year | |

| Total take up | 230,730 | 450,627 | -48.8% | -45% |

| Prime take up | 7,853 | 79,406 | -90.1% | -49.2% |

| Secondary take up | 222,877 | 371,221 | -40% | -29.4% |

Significant occupational transactions

| Property | Size | Landlord | Tenant | Terms | Rent/Price (per sq ft) |

| Unit H2 Hazleton Interchange, Waterlooville | 25,812 sq ft | IPIF | Formaplex | 10 year lease | £8.50 |

| Unit 2 iO Centre, Segensworth | 16,714 sq ft | Forelle Estate Limited | Anglian Windows Limited | 10 year lease | £8.00 |

| Unit 2 Alpha Park, Chandlers Ford | 44,868 sq ft | Blackrock | Charles Kendall Freight | 10 year lease | £10.00 |

| Unit 3 A Dunsbury Park Havant |

11,300 sq ft 1.3 acres |

Portsmouth City Council | VW Breeze | 20 year lease | £9.25 + overage |

| Unit 1 Davis Way, Fareham | 9,715 sq ft | Hargreaves (Trading Property) Ltd | Funeral Services Limited | 20 year lease | £8.00 |

| Unit 4 (Business Hanger) Solent Airport, Daedalus | 6,394 sq ft | Fareham Borough Council | Phoenix Helicopter Academy | 6 year lease | £7.75 |

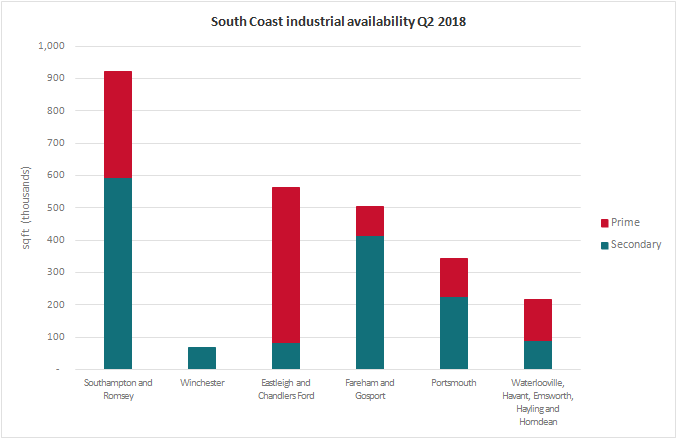

Secondary stock at lowest levels since 2015

Grade A stock continues to rise out of the ground and near completion, rejuvenating the industrial stock on the South Coast, as it continues to be a key location for national and international occupiers as well as home to local occupiers. Notable newly available developments in the region include Units 5 and 6 Mountpark, Southampton totalling 167,150 sq ft and Units 1 – 3 Velocity, Havant together some 101,726 sq ft, and Merlin Park, Portsmouth of 7 units totalling 91,000 sq ft complementing the completed schemes Alpha Park, Chandlers Ford and South Central Nursling.

The majority of the schemes have been brought forward to satisfy the mid box / big box requirements, however there is now a real shortage of prime stock for smaller units presenting a gap in the market for developers to satisfy. One success story of this is take up at Glenmore Business Park, Chichester where Glenmore has built 75 small business units.

Availability of secondary stock continues to decline dropping to its lowest level since Q3 2015, although overall availability is on the rise.

The vital statistics have been summarised below:

| Q2 2018 (sq ft) | Q1 2018 (sq ft) | % change | % change Year on Year | |

| Total stock | 2,616,679 | 2,433,300 | 7.5% | 17.2 |

| Prime stock | 1,138,217 | 907,227 | 25.5% | 82.3 |

| Secondary stock | 1,478,462 | 1,526,073 | -3.1% | -8.1 |

Double Digits Reached

| Under 5,000 sq ft | Prime capital value per sq ft | Prime headline rent per sq ft | Secondary capital value per sq ft | Secondary headline rent per sq ft |

| Portsmouth and Havant | £135 - £145 | £10.00 | £90 - £100 | £8.50 |

| Southampton and Eastleigh | £150 - £160 | £12.00 | £90 - £100 | £10.00 |

| Bournemouth and Poole | £140 - £150 | £9.50 | £95 - £105 | £8.50 |

| 5,000 - 20,000 sq ft | Prime capital value per sq ft | Prime headline rent per sq ft | Secondary capital value per sq ft | Secondary headline rent per sq ft |

| Portsmouth and Havant | £125 - £135 | £9.50 | £70 - £80 | £8 |

| Southampton and Eastleigh | £130 - £140 | £9.50 | £80 - £95 | £9.00 |

| Bournemouth and Poole | £115 - £120 | £8.50 | £85 - £95 | £7.50 |

|

Over 20,000 sq ft |

Prime capital value per sq ft | Prime headline rent per sq ft | Secondary capital value per sq ft | Secondary headline rent per sq ft |

| Portsmouth and Havant | £110 - £130 | £9 | £70 - £80 | £7.75 |

| Southampton and Eastleigh | £115 - £140 | £10.00 | £70 - £85 | £8.75 |

| Bournemouth and Poole | £110 - £120 | £8.25 | £65 - £75 | £7.25 |

Investment Market Review

Related Content

REGISTER FOR UPDATES

Get the latest insight, event invites and commercial properties by email